The

when-to-sell decision has always been more difficult than the when-to-buy

decision because the decision to buy only needs two conditions. We need to have

the free cash and we need to have a compelling story. The when-to-sell decision

has always been a historical nightmare for both professional and private

investors because there are too many moving parts to consider. We have the

micro or bottom up worries such as the compelling storey that has suddenly gone

sour. Perhaps some chart pattern has negative implications. We also have the

emotional baggage that compels us to sell a winner too soon and to hold on to a

loser too long.

We

also have the macro or top down worries such as the current crisis be it the

never ending Euro-Zone problems or the threat of a slowing Chinese economy. Now

we have the mindless chirping of the seasonal “sell” crowd pressuring investors

into switching a good portion of their equity portfolios to cash.

The

root of the problem is the failure to have an exit strategy in place at the

time of the decision to buy. The exit strategy or stop loss option should never

be based on changing fundamentals, otherwise known as the “compelling story”

because the price decline will often lead the deteriorating business model. I

am sure long tem investors in the shares of Nortel Networks Corporation or

Research In Motion Limited would agree with this observation

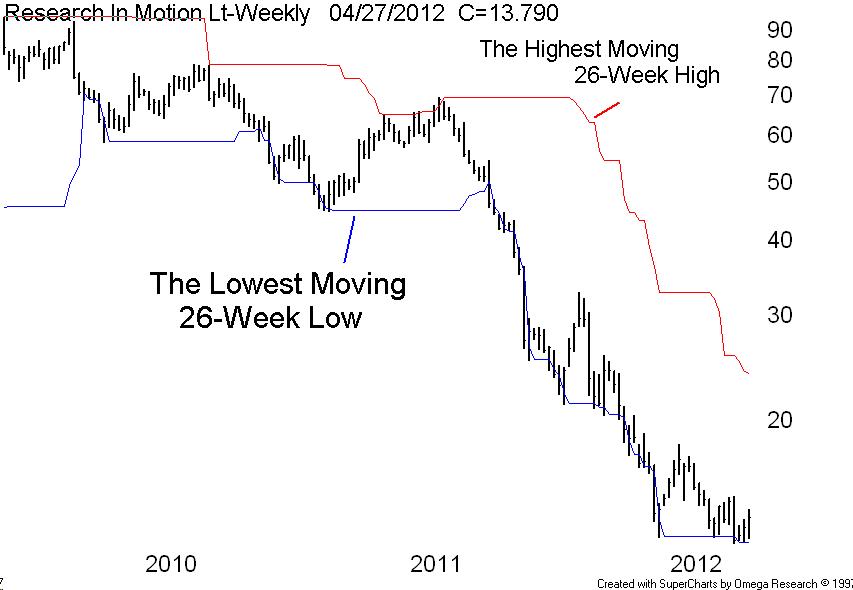

The

Lowest 26-Week Low is a simple strategy with no math required. Set your stop at

the lowest low of the past twenty six weeks. This is a moving 26-week window,

so each week add the new week and drop the oldest week. Sell if the weekly

price closes below the prior lowest 26-week low. Conversely, if the price is

rising the lowest 26-week low will follow the stock upward which allows us to

hold a rising stock in some cases for weeks, months or years.

Our

chart this week is that of the weekly closes of Research In Motion plotted

above the lowest 26-week low price channel. Note the numerous price declines

below the 26-week price channel trough 2010 and 2011. No excuses for big losses

here.