Dominant

theme investing has been my focus for the last several years starting with the “echo”

technology boom and then on to lumber and now aerospace. These sectors are

still in youthful secular bull phases.

Below

is the text I authored and published by the Toronto Star business on or about September

7, 2013.

----------------------------------------------------------------------

Traditionally

financial planners and investment advisors have embraced two basic rules when

advising clients on personal finance and equity investing

Never

get divorced, and never buy an airline stock.

The

never buy an airline stock rule is deep rooted and for good reason.

Investors

have long nightmare like memories when it comes to the North American airline

industry. In Canada we have

infamous names like Air Canada,

Wardair. Canadian Airlines, Zoom Airlines and Canada 3000. In the U.S. the list

is too long for this space.

Industry

experts have blamed the carnage on de-regulation, rising fuel costs, security

costs and various global crises such as the technology bubble of 2000 and the

financial crisis of 2008.

The

AMEX Airline index (XAL) which is designed to measure the performance of highly

capitalized companies in the commercial airline industry peaked in 2000 at the

160 level. By March 2009 the XAL was trading at the 16 level for a stunning

loss of 90 per cent,

The

dismal performance of the XAL is in sharp contrast to the success of the

related commercial and defence manufactures and contractors. Names like he

Boeing Company (BA), Honeywell International Inc. (HON) and United Technologies

Corp. (UTX) are trading close to recent all-time highs.

Most

notable is the list of the top North American manufacturing employers. Names

like General Electric Company, General Motors Company, United Technologies

Corp, Ford Motor Co., The Boeing Company, Lockheed Martin Corporation and

Honeywell International Inc. are all related to trains, planes and automobiles,

The

common theme among most of these names appears to be related to aerospace and

made in North America.

Loosely

defined, aerospace is branch of technology and industry that is shared by three

major components, the defence industry, commercial aviation and space

exploitation programs such as spaceships and satellites.

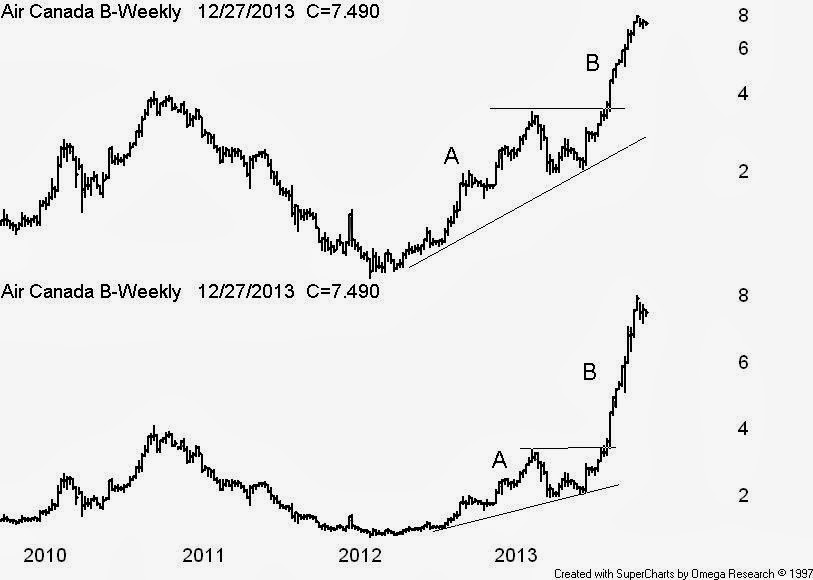

Bullish

Investors in the aerospace sector have lately chosen to ignore that never buy

an airline stock rule. In the U.S.

the AMEX Airline index has soared 300 per cent from the March 2009 lows and

locally Air Canada

and WestJet Airlines Ltd, were among the top performers on the TSX in 2012.

According

to Standard & Poor's Capital IQ global air traffic trends are looking

positive. They claim the underlying drivers of the commercial aerospace

industry are improving global economic growth, an emerging global middle class

and the upgrade of an aging fleet of commercial aircraft.

The

commercial and defence manufactures are awash with orders from airlines

switching to new aircraft.

Some

recent Canadian examples would be WestJet Airlines Ltd (WJA) reaching a

preliminary agreement to purchase 65 737 MAX aircraft from Boeing Co (BA), and

Bombardier Inc. (BBD.B) recently signing a letter of intent to sell 50 Q400

NextGen turboprop aircraft to the Russian state-owned industrial and defence

conglomerate Rostec.

If

an investor embraces the aerospace theme he or she will need to seek out the

companies or investment products that will provide some exposure to the sector

In

other words we need to engage in stock picking or seek out sector related

exchange traded funds (ETFs).

At

the moment there appears to be no commercial airline industry ETFs that would

track the AMEX Airline index (XAL). Guggenheim Investments closed nine ETFs

back in March 2013 due to lack of investor interest. One of them was the

Guggenheim Airline ETF (FAA) which could be goods news to a contrarian

investor.

In

the U.S.

there are several ETFs that will provide direct exposure to all components of

the aerospace sector.

The

NYSE listed iShares Dow Jones US Aerospace & Defence ETF (ITA) tracks the

Dow Jones U.S. Select Aerospace & Defense Index. It has 33 holdings, to

include stocks like United Technologies Corporation (UTX), Boeing (BA),

Goodrich Corporation (GR) and Lockheed Martin (LMT).

Also

listed on the NYSE is the PowerShares Aerospace & Defence ETF (PPA) which

tracks the SPADE Defense Index. It has 51 holdings, to include Honeywell

International (HON), United Technologies Corporation (UTX), Lockheed Martin

(LMT) and Raytheon Corporation (RTN).

Here

in Canada

the ETF manufactures have avoided the space and so we have to engage in stock

picking.

Currently

there are only five TSX listed companies in the aerospace sector, CAE Inc.

(CAE), Magellan Aerospace Corporation (MAL), Bombardier Inc. (BBD.B),

MacDonald, Dettwiler and Associates Ltd. (MDA) and Héroux-Devtek Inc. (HRX)

Some

of these names may not be suitable investments and you may need the advice of a

fully licensed advisor before making an investment decision.