Google “The Dow Industrials 1929 vs 2010” and you end up with pages of historical comparisons between the Crash and rebound of 1929 and the current “rally”. David Rosenberg economist and strategist for Gluskin Sheff + Associates Inc., and a guest columnist for Report on Business authored yet another comparison item entitled “Current rally has echoes of 1930 snapback” Wednesday's Globe and Mail March 31, 2010. I initially brushed off the item to be just another bear (who has missed out on the big 2009-2010 advance) who is arguing with the markets in a public forum but the weak technical arguments grabbed my attention and I quote.

“Not only is the U.S. equity market overvalued by more than 25 per cent, it is also extremely overbought, having gone 24 sessions without a decline of 1 per cent or more. Moreover, 89 per cent of the stocks in the S&P 500 are now trading above their 50-day moving averages - and volume remains tepid at best.”

And:

“From our lens, the rally of the last 12 months smacks of the 1930 snapback, and if I'm not mistaken the S&P went on to hit new lows in subsequent years and the next secular bull market did not start until 1954.”

And:

“The theory that the stock market has turned in a "double top" may not have gone the way of the dodo bird after all, following the reversals we saw in the last two trading days of last week”.

Before I continue we need a little background on the structure of the 1929 Crash. The Dow entered the “Roaring Twenties” running up non-stop from an October 1923 low of 85.70 to peak at 381 In September 1929. From there the Dow plunged 48% to 198 in just 71 days to bottom in November 1929. The following recovery wave – or bear market rally lasted 155 days to peak at 294 on April 1930 for a gain of 48%. The final down wave lasted 800 days taking the Dow to a low of 41 in July 1932 for a loss of 86%.

In terms of Elliott Wave we had an A-B-C corrective bear with the low at C (July 1932) the point of origin for the famous 20th century Supercycle Wave as set out in the respected publication -

Elliott Wave Principle by Frost and Prechter. In other words the July 1932 low was the Buy-of-the-Century. I should also mention that Rosenberg refers to the S&P which was not published until 1957.

Ok now I admit to being no match for Rosenberg the economist although I did study Paul A. Samuelson’s –

Economics An Introductory Analysis at my first year at Ryerson University but - I also studied the works of Ian S. Notley, Martin Pring, Frost & Prechter and John J. Murphy. Now if there is one thing history has taught me about the capital markets it would be - an economist should never manage money - because they are always mucking about in ancient data that has no relevance to the equity markets that are always pricing “valuations” on what will happen and not on what has happened.

First lets examine the “From our lens” stuff with the overbought comment and the observations relating to the 50-day moving averages. The 50-Day MA is a trading tool that generates over-bought and over-sold signals about every 15 days and an experienced technician would never compare a short term trading condition to a much larger November 1929 to April 1930 recovery wave that spanned 155 trading days

Next Rosenberg supports the theory that the stock market has turned in a "double top" – sorry but where? Would that be the 2000 and 2007 peaks of the S&P500? Certainly not the Dow Industrials, the Dow Transports, the Russell 2000 or the TSX Composite. Now about those reversals we saw in the last two trading days of last week (I assume the week ending March 26, 2010). One day reversals are for day traders. Is Rosenberg actually using a one day reversal to support his “echo of 1930 theory?

Now I think Rosenberg’s economic arguments have merit when he claims - “the current rebound in the economy is a statistical mirage orchestrated by record amounts of monetary and fiscal stimulus that are simply unsustainable and actually risk precipitating a very unstable financial and economic backdrop in coming years.” I do however think Rosenberg is getting poor advice on the technical side because to-day’s technical picture has no relevance to the 1929 – 1932 technical structure.

The 1929–1932 bear was of 34-months in duration and we are now into month 30 following the last modern October 2007 bull peak of the S&P500. That means to-day’s S&P500 has only 4 months to fall from the current 1178 level to below the March 2009 low of 666 in order to mirror or “echo” the 1929-1932 bear. In addition the current “flashy bear market rally” is in fact a bull market because we are into month 13 above the March 2009 low. No bear market has ever failed to break to new lows within a 12 month window.

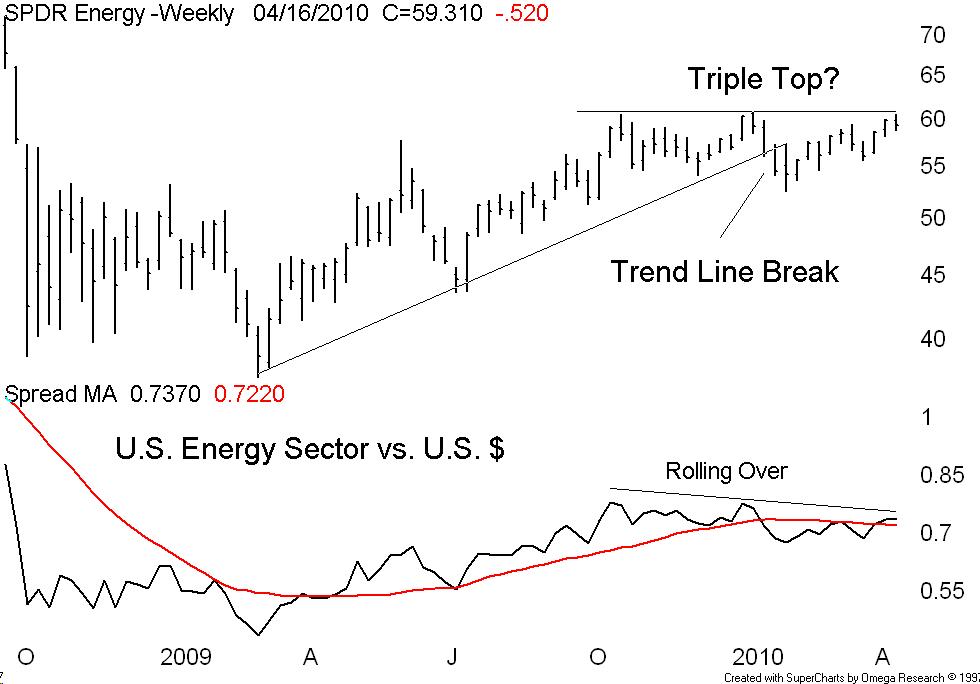

The real technical problem (too bad Rosenberg never gave me a call) is the price of crude pushing above $80. Note the long term monthly chart of the Dow Industrials plotted above the price of crude and note the modern trading range of crude the North American markets can tolerate because of peaking crude consumption due to alternate sources and more fuel efficient autos combined with muted long term growth prospects. Forget 1929 – right now the last thing we need is another 1973 style energy price shock